SINGAPORE (EDGEPROP) – The Central Region office rents posted its first correction since turning around in 3Q17. showed the Urban Redevelopment Authority (URA) statistics. JLL commenting on this price correction in the Central Region office rents said the government data runs contrary to JLL’s observation of “rent growth accelerating in 1Q19 across almost all submarkets tracked.”

Specifically, JLL’s research showed that the average monthly gross effective signing rents for a fixed basket of Grade A office assets in the CBD rose 3.7% q-o-q in 1Q19 to SGD 10.63 per sq ft from SGD 10.25 per sq ft in 4Q18. This is faster than the 3.3% q-o-q recorded in 4Q18 and 2.3% q-o-q recorded in 3Q18.

The relentless rise in the rents of the basket of office assets tracked by JLL was underpinned by diminishing availability of good quality office space in the CBD for lease amid firm demand and limited new supply.

Commenting on the price correction in the Central Region office rents, Ms Tay Huey Ying, JLL’s Head of Research and Consultancy for Singapore, said:

“The correction reflected in URA’s 1Q19 office rental index could be due to the occurrence of more leases taking place in Category 2 offices as the availability of Category 1 offices for lease diminishes amid firm demand. A more active Category 2 office leasing market could have dragged down the overall rental index for the quarter.”

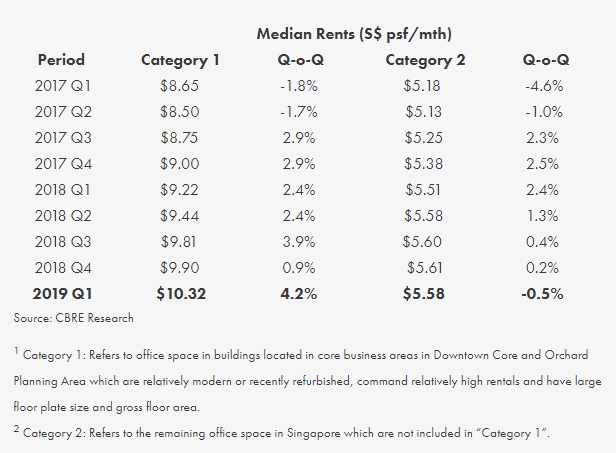

“Category 1” refers to office space in buildings located in core business areas in Downtown Core and Orchard Planning Area which are relatively modern or recently refurbished, command relatively high rentals and have large floor plate size and gross floor area while “Category 2”, refers to the remaining office space in Singapore which are not included in “Category 1”.

Ms Tay added: “JLL remains upbeat about the prospects for Singapore’s office leasing market given steady demand for office space as evidenced by the healthy pre-commitments for schemes scheduled for completion in 2019, namely 9 Penang Road and Funan. This is amid tight vacancy of 6.0% for Grade A office space in the CBD as of the end of 1Q19 which we expect to tighten further to below the frictional rate of 5% by the end of 2019.”

JLL maintains that supply squeeze will continue to give landlords the upper hand in lease negotiations. It said, “barring adverse external shocks, there is potential for 2019 to outperform 2018 in terms of rent growth for Grade A office space in the CBD.”

JLL’s research showed that the average monthly gross effective rents of Grade A office space in the CBD rose 11.8% in 2018, faster than the 7.7% staged in 2017.

Besides the price correction of the Central Region office rents which dipped after rising for six consecutive quarters, sales prices and vacancy of office properties continued to recover in Q1 2019, noted Colliers International.

Like JLL, Colliers too suggested that rents of CBD Premium Grade A and Grade A offices are still rising. It believes that the drag in the Central Region office rents could be attributed to office buildings outside the basket of properties tracked by Colliers.

Colliers noted that, “URA’s Office Rental Index for the Central Region is 8.6% below the most recent peak in Q1 2015.” Adding: “Nonetheless, island-wide vacancy as tracked by URA declined 0.3ppt QOQ to 11.8% during Q1 2019, as net demand expanded from a broad range of sectors.”

Mr Desmond Sim, Southeast Asia’s Head of Research for CBRE said, the Central Region office rents correction could be due to the contrasting performances of good quality office buildings in the core CBD versus those of the older and less well-located offices. He added that the lower rentals achieved in the non-core business areas likely contributed to the weaker performance of the overall rental index.

CBRE’s data showed that the median rents for Category 11 offices grew at a robust pace of 4.2% q-o-q. On the other hand, the median rents for Category 22 offices, where growth has been tapering, saw a 0.5% decline.

Mr Sim said, “Islandwide vacancy fell to 11.8%, supported by net absorption of 19,000 sq m. While relatively healthy, it is noteworthy that leasing has been mainly driven by technology and, in particular, co-working operators. Should these sectors be excluded, the underlying strength of occupier expansion is less convincing.”

He added: “The office outlook remains fairly positive for now. With very decent pre-lease commitments already in place and a tapering supply pipeline, landlords’ strong leverage is likely to be maintained. That said, we are seeing some occupier resistance to the pace of rental increases, with negotiations for renewal and relocation becoming more protracted.”

If you are looking to sell or purchase properties in Singapore, our team members can help you with Affordability Assessment and Asset Progression Plan. Call us now at +65 86666 944 or +65 9844 4400